By Susan Boskey

By Susan BoskeyPeople tend to increase spending when the prices of their stock market and real estate assets rise. They perceive it as an increase to their financial security. This is known as the wealth effect.

The wealth effect is a psychological phenomenon that causes people to spend more as the value of their assets rises. The premise is that when consumers’ homes or investment portfolios increase in value, they feel more financially secure, so they increase their spending. Conversely, when consumers see the value of their homes or portfolios fall, they tend to spend less. The wealth effect attempts to explain why consumers might change their spending habits even if their income and fixed costs have stayed the same. ~ InvestopediaMonetary policymakers consider the increased consumer spending that follows a rise in the price of assets to be an indicator of economic recovery. But is it really and does the everyday family benefit? What is the reality?

- Higher home prices (significantly increased since 2008) make home ownership more unavailable to more people. Home ownership is at its lowest rate since tracking began in 1963.

- Higher home prices also put rental property prices out-of-reach to more people.

- Home sales in 2016 are not broad-based and people-driven as they were in 2008, albeit via sub-prime loans. Now a large percentage of homes sales are cash sales of homeowners and investors (domestic and foreign) who need somewhere to park assets. Banks offering low interest rates remain an unattractive option.

- Additionally, the 2016 big bump in home sale prices and purchases are pocketed in 3 main areas of the United States due to the presence of the U.S Government, government contracts, and technology companies: Washington D.C., New York, and San Francisco where tech employees can get home loans based on their stock option prices.

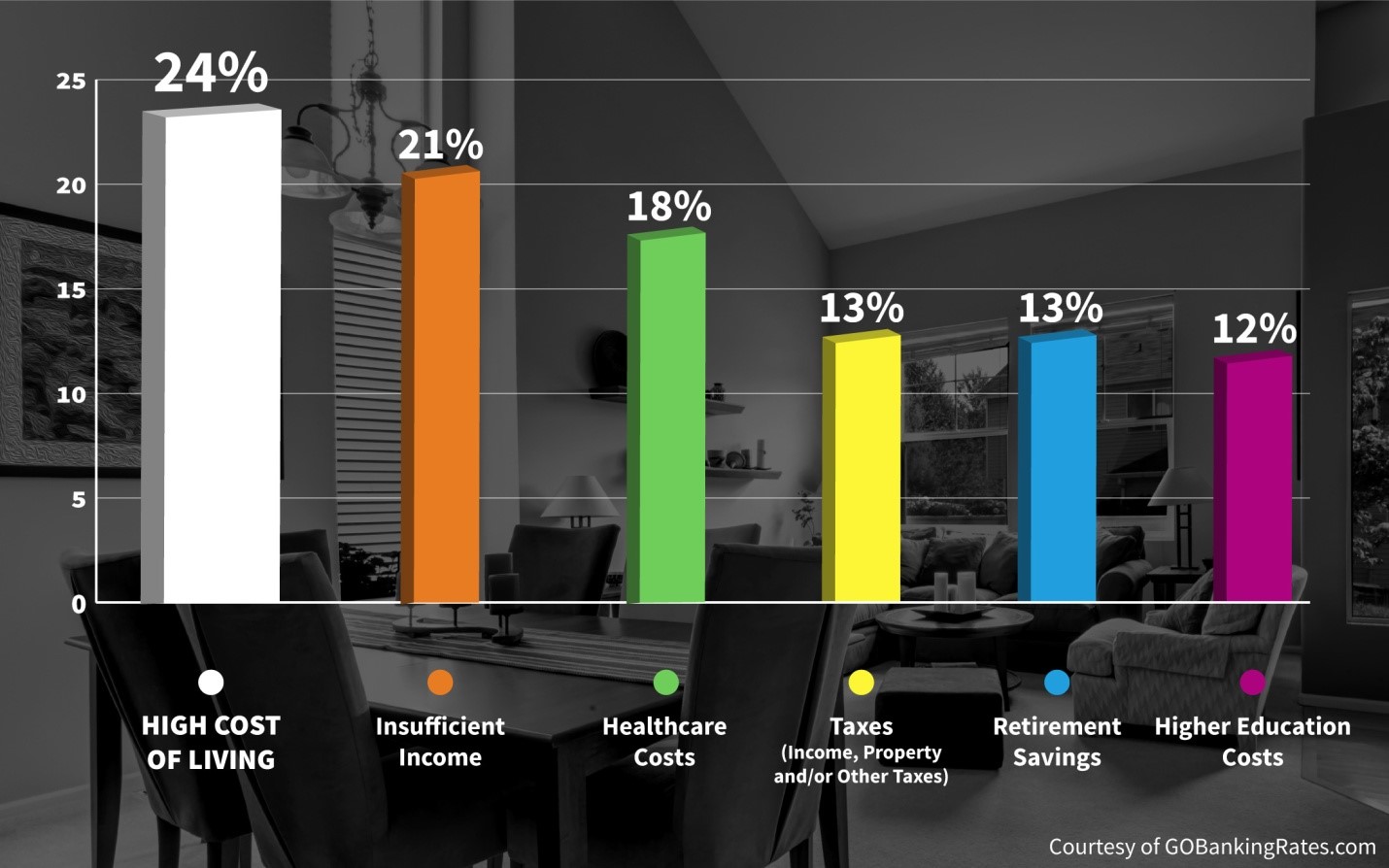

- High cost of living

- Healthcare costs

- Insufficient income

- Taxes (income, property, and/or other taxes)

- Retirement savings

- Higher education costs

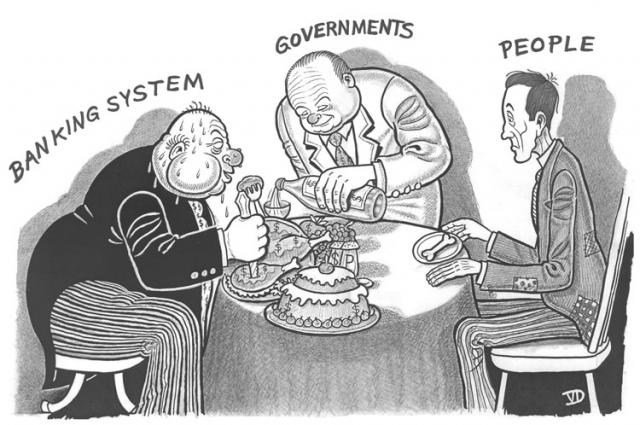

The wealth effect is a smokescreen. It distracts from any focus being put on the flaws of the monetary system. Rising asset prices favor the haves who own assets (minority), while extracting precious resources from the have-nots (majority).

More decent-paying jobs can certainly help; but alone, jobs cannot make it “right.” Why? The independent-of-governments central banking system pulls the strings. Simply put: The money they issue is systemically devalued via a mathematical formula decreasing money’s purchasing power. Anyone who has studied this, as I have, knows that nothing short of a system overhaul could possibly bring back long-term economic recovery. Even if everyone had a job, their hard-earned money over time will purchase less and less.

The good news is that by this knowledge you can rethink the best ways to earn, spend, save and invest to ensure the most quality in your life with the least amount of stress. That is, until really real change takes place at the monetary system level.

Susan Boskey is author of the book, The Quality Life Plan®: 7 Steps to Uncommon Financial Security. After exposing the bottom-line of why more and more families need credit each month just to make ends meet, Susan provides game-changing practical strategies, tactics and templates to help you create a life of greater ease. You can reverse the downward trend of credit and debt while learning how to establish a long-term, debt-free lifestyle; a life that allows you to build both financial wealth and the wealth of well-being midst the challenges of today’s economic landscape. To learn more or to purchase the book, please visit her website at http://TheQualityLifePlan.com

Susan can customize her strategies and templates for your particular situation and is available to coach you through this process. She can be reached through her website.