“La sabiduría de la vida consiste en la eliminación de lo no esencial. En reducir los problemas de la filosofía a unos pocos solamente: el goce del hogar, de la vida, de la naturaleza, de la cultura”.

Lin Yutang

Cervantes

Hoy es el día más hermoso de nuestra vida, querido Sancho; los obstáculos más grandes, nuestras propias indecisiones; nuestro enemigo más fuerte, el miedo al poderoso y a nosotros mismos; la cosa más fácil, equivocarnos; la más destructiva, la mentira y el egoísmo; la peor derrota, el desaliento; los defectos más peligrosos, la soberbia y el rencor; las sensaciones más gratas, la buena conciencia, el esfuerzo para ser mejores sin ser perfectos, y sobretodo, la disposición para hacer el bien y combatir la injusticia dondequiera que esté.

MIGUEL DE CERVANTES Don Quijote de la Mancha.

La Colmena no se hace responsable ni se solidariza con las opiniones o conceptos emitidos por los autores de los artículos.

5 de junio de 2015

Half of All American Families Are Staring at Financial Catastrophe

And they’re turning to payday loans and other lenders of last resort when crises occur.

The most frightening finding in the Federal Reserve’s Report on the Economic Well-Being of U.S. Households in 2014 concerns a matter of $400. Four-hundred bucks. Twenty twenties. Four Benjamins.

Or just enough to crush half of all American households.

“Forty-seven percent of respondents say they either could not cover

an emergency expense costing $400, or would cover it by selling

something or borrowing money,” reads this year’s annual report.

Maybe Americans are feeling better about their finances, as The Wall Street Journalputs

it, but that figure is a downer. Several years into the recovery,

almost half of all U.S. households could not withstand a minor financial

shock without incurring debt or liquidating assets.

“Even prior to

the [Great Recession], and more acutely after the recession, it’s true,

American households are vulnerable,” says Gregory B. Mills,

senior fellow at the Urban Institute. “Depending upon the measure you

use, somewhere between one-third and one-half of households are at great

risk—as in, they would be unable to fend off hardship.”

Families’ savings not where they should be: That’s one

part of the problem. But Mills sees something else in the recovery

that’s more disturbing. The number of households tapping alternative

financial services are on the rise, meaning that Americans are turning

to non-bank lenders for credit: payday loans, refund-anticipation loans,

pawnshops, and rent-to-own services.

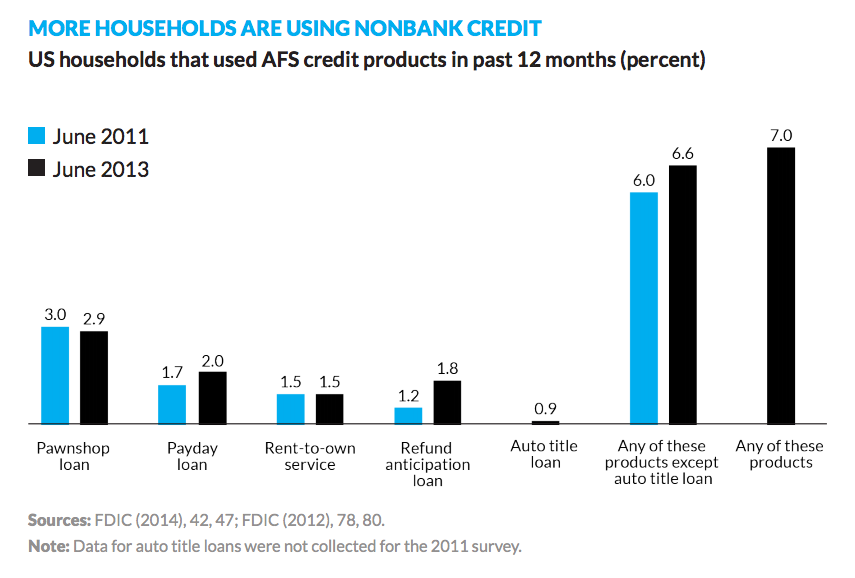

According to the Urban Institute report,

the number of households that used alternative credit products

increased 7 percent between 2011 and 2013. And the kind of household

seeking alternative financing is changing, too.

(Urban Institute)

While that

figure might seem small—it’s an increase of about 750,000 households

total—it’s a significant figure for the economy in recovery. Families

that are looking for credit aren’t finding it in mainstream financial

institutions. “You used to be able to get small loans for reasonable

rates, below 36 percent,” Mills says. “That’s what’s opened the door for

more predatory products.”

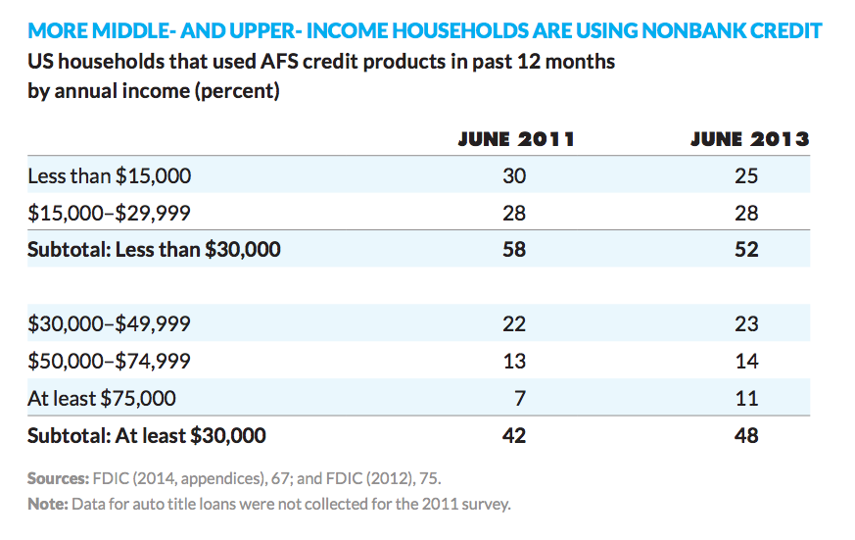

The nature of households looking for alternative financial

products, including predatory loans, has morphed during the recovery.

According to Mills’s research, the share of households seeking non-bank

credit with incomes above $30,000 increased from 42 to 48 percent

between 2011 and 2013. And the share making more than $75,000 increased

from 7 to 11 percent over the same span.

(UrbanInstitute)

It’s not the

case that every one of these middle- and upper-class households turned

to pawnshops and payday lenders because they got whomped by an

unexpected bill from a mechanic or a dentist. “People who are in these

[non-bank] situations are not using these forms of credit to simply

overcome an emergency, but are using them for basic living experiences,”

Mills says.

Still,

survey respondents who said they couldn’t weather a $400 hit are bound

to be some of the same folks who are turning to non-bank lenders for

routine expenses. That’s a huge problem nationwide. Alternative

financial services come with steep interest rates, especially payday

lenders, which lock borrowers into vicious lending cycles with interest

rates north of 400 to 500 percent. The Consumer Financial Protection Bureau is moving to regulate the payday lender sphere—which is a good start.