“La sabiduría de la vida consiste en la eliminación de lo no esencial. En reducir los problemas de la filosofía a unos pocos solamente: el goce del hogar, de la vida, de la naturaleza, de la cultura”.

Lin Yutang

Cervantes

Hoy es el día más hermoso de nuestra vida, querido Sancho; los obstáculos más grandes, nuestras propias indecisiones; nuestro enemigo más fuerte, el miedo al poderoso y a nosotros mismos; la cosa más fácil, equivocarnos; la más destructiva, la mentira y el egoísmo; la peor derrota, el desaliento; los defectos más peligrosos, la soberbia y el rencor; las sensaciones más gratas, la buena conciencia, el esfuerzo para ser mejores sin ser perfectos, y sobretodo, la disposición para hacer el bien y combatir la injusticia dondequiera que esté.

MIGUEL DE CERVANTES Don Quijote de la Mancha.

La Colmena no se hace responsable ni se solidariza con las opiniones o conceptos emitidos por los autores de los artículos.

13 de septiembre de 2016

Traders Bemoaning Lack of Shock, Awe in Markets Finally Get Some

Friday’s selloff has traits common with past volatility shifts

Investors enduring a third day of elevated turbulence.

Traders

who complained all summer about markets stuck in a zombie state are

getting what they wanted, and probably will be for a while.

Eruptions

of volatility this big rarely go away quickly. By one measure, the

selloff ripping equities represents the sixth most violent rupture to

market calm in history, with the S&P 500 Index’s drop of 2.5 percent

exceeding its daily move in the prior month by a factor of 10. Every

time that happened in the past, turbulence took its time petering out.

Patterns

like that may affirm the view of bears who spent July and August

warning that the peace blanketing everything from equities to bonds and

currencies was likely to end in a bang, not a whimper. Of particular

concern right now is the concerted nature of the selloff in which

markets that don’t ordinarily move in the same direction suddenly are.

“When

investors come back from the beach and start thinking about, ‘How am I

going to prepare for the fourth quarter?’ we’re going to see a lot of

activity,” said Brad McMillan, chief investment officer of Commonwealth

Financial Network in Waltham, Massachusetts, which oversees $100

billion. “Volatility doesn’t go away. It gets stored up.”

Stocks

and bonds plunged in tandem for the second time since Friday, driving

measures of volatility higher as investors lost confidence central banks

still have ammunition to promote growth. U.S. stocks notched their

third straight move of at least 1 percent after 43 days without one,

while Treasury yields were jolted out of the tightest monthly range in a

decade. Oil joined the selloff, punishing currencies of resource

exporters and leaving investors with few places to hide.

Among the pressure points:

Lockstep

drops. A gauge tracking hedge fund strategies that balance bets over

markets, the Salient Risk Parity Index, plunged the most since August

2015 on Friday.

Tepid data. Bloomberg’s index of economic surprises turned negative for the first time since July.

Earnings

estimates. Analysts see S&P 500 profits falling 1.4 percent in the

third quarter, almost double the drop they saw a month ago.

“People

are certainly on edge around here,” said Robert Pavlik, who helps

oversee $9.1 billion as chief market strategist at Boston Private

Wealth. “The one saving grace is that we as a firm have some cash on the

sidelines, but that doesn’t do any good when you’re still 90 percent

invested in equities. You can’t help but feel some pain.”

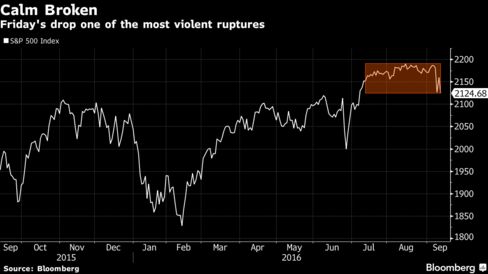

Two

months of tranquility was pierced Friday when the S&P 500 tumbled

in its worst rout since the U.K. voted to leave the European Union.

Angst as measured by the CBOE Volatility Index climbed 21 percent as of 4

p.m. in New York Tuesday after increasing Friday by 40 percent, its

biggest gain in three months.

Things aren’t any better in the

$13.6 trillion Treasury market. Ten-year notes were stuck in their

tightest monthly range in a decade up until September, while implied

volatility in global currencies was near the lowest this year before

surging at the quickest pace since the June 23 Brexit referendum, a

JPMorgan Chase & Co. index showed.

For bond traders at Pioneer

Investment, the stress represents vindication. The firm has been

betting against longer-dated Treasuries, a losing trade for most of this

year until last week.

“We were very pleased that the strategy

finally seems to be working,” Paresh Upadhyaya, director of currency

strategy in Boston at Pioneer, which oversees about $236 billion. “Is

the global rise in yields a structural change, meaning we’ve seen the

bottoming in yields or is this another head-fake that’s roiled

fixed-income from time to time? This time feels different.”

Stocks

exited the tightest trading range in history last week when European

Central Bank President Mario Draghi downplayed the need for more

measures to boost growth and Boston Fed President Eric Rosengren warned

against waiting too long to raise interest rates. While equities

rebounded after Fed Governor Lael Brainard urged prudence in raising

rates, they succumbed anew Tuesday with valuations sitting near the

highest level in more than a decade.

“Everyone

was out for the summer. Now all of a sudden people are asking ‘Are they

going to raise interest rates?”’ said Bruce Campbell, fund manager with

StoneCastle Investment Management in Kelowna, British Columbia. His

firm manages about C$100 million. “People were running out on Friday,

then they were running back in yesterday, now they’re running for the

exits again today. It’s a crazy, bipolar stock market.”Such

abrupt breaks in calm have not been easily resolved in the past. In the

five prior instances when turbulence spiked as it did Friday, the

S&P 500’s daily swings averaged 1.5 percent in the next 20 days.

That’s 2.5 times the move in the previous 20 days, data compiled by

Bloomberg and Bank of America Corp. show.

Markets

look fragile, Bank of America analysts led by Abhinandan Deb wrote in a

note to clients Tuesday. “We believe a bona fide bond shock remains a

key destabilizing risk to markets, particularly if catalyzed by a loss

of confidence in central banks.”

It’s

been a while since a protracted decline took hold. Following Britain’s

decision to exit the European Union, the S&P 500 dropped 5.3 percent

over two days, only to rally the next four and erase the entire plunge

two weeks later. Two 10 percent corrections that began in August 2015

and January 2016 also proved short-lived.

That’s

not to say that stocks will follow the same route this time. With

S&P 500 profit in the worst decline since 2009 and presidential

elections looming, the list of reasons for the second-longest bull

market to strengthen is getting shorter. While improved economic data

helped fuel the S&P 500’s 20 percent rally from a February low,

signs of weakness are emerging.

All year

bulls have pointed to an element missing from market psychology and

said it would prevent a full-blown selloff -- overconfidence. But signs

of exuberance have been multiplying in the market, including record high

levels of bullish holdings by hedge funds in index futures contracts

and unrepresented short positions in VIX futures.

“There

is just this steady crowding into stocks because that’s the only place

to generate returns. That’s a pretty complacent approach,’’ said Eric

Schoenstein, Portland, Oregon-based co-manager of the $5.4 billion

Jensen Quality Growth Fund. “When you take your eyes off the potential

for risk, that’s when you can really get harmed as an investor.’’