by Ben Sharples and Perry Williams

-

Al-Falih says Saudis to cut ‘substantially’ below agreed level

-

Non-OPEC countries agree to trim output 558,000 b/d next year

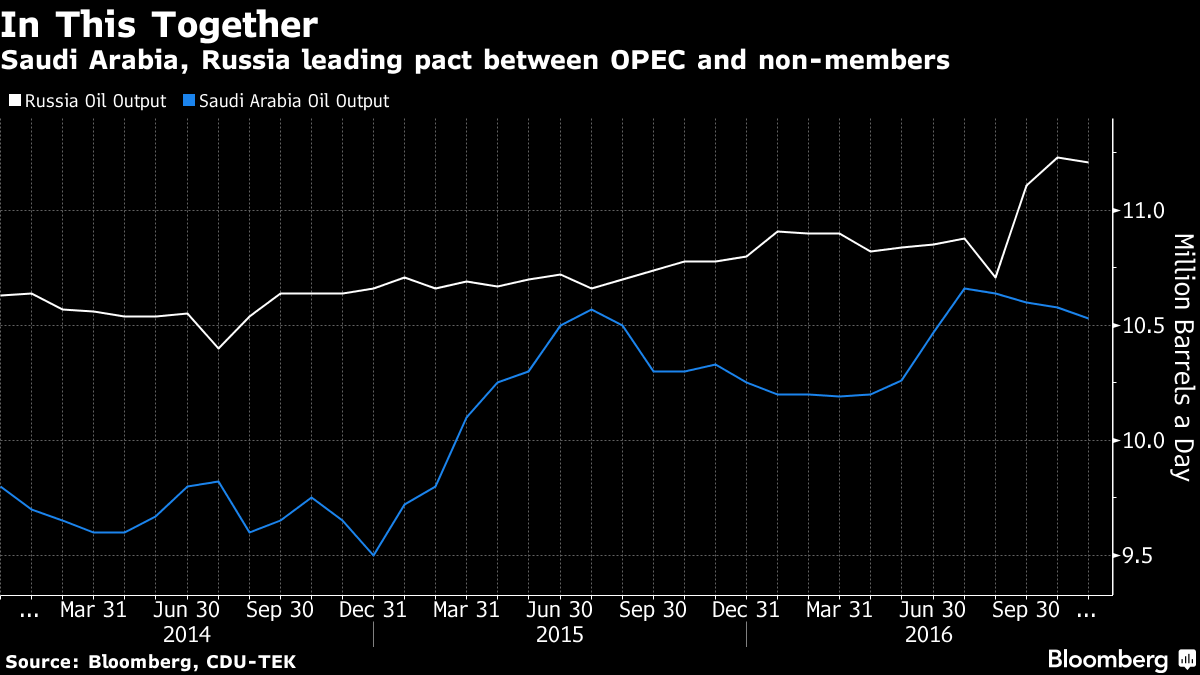

Oil jumped to the highest since July 2015 after Saudi

Arabia signaled it’s ready to cut output more than earlier agreed while

non-OPEC countries including Russia pledged to pump less next year,

strengthening the coordinated commitment by the world’s largest

producers to tighten supply.

Futures rose as much as 5.8 percent in New York and 6.6

percent in London. Saudi Energy Minister Khalid Al-Falih said Saturday

the biggest exporter will “cut substantially” below the target agreed to

last month with members of the Organization of Petroleum Exporting

Countries. Al-Falih’s comments followed a deal by non-OPEC countries

to join forces with the group and reduce production by 558,000 barrels a

day next year, the first pact between the rivals in 15 years.

“This is a very powerful message that producers want to balance the market higher,” said Chris Weston, chief market strategist in Melbourne at IG Ltd. “As a statement of intent, this is about as bullish as it gets.”

West Texas Intermediate for January delivery rose as much as $3.01 to $54.51 a barrel on the New York Mercantile Exchange, the highest intraday level since July 6, 2015. The contract was trading at $54.05 at 7:35 a.m. Hong Kong. Prices gained 3.5 percent over the previous two sessions to close at $51.50 a barrel on Friday.

Brent for February settlement rose as much as $3.56 to $57.89 a barrel on the London-based ICE Futures Europe exchange. The global benchmark crude traded at a $2.02 premium to February WTI.

“Assuming reasonable compliance levels, these cuts will be enough to push the market into deficit,” said Neil Beveridge, a senior analyst at Sanford C. Bernstein in Hong Kong. “This level of coordination is unprecedented.”

Saudi, Russia

"I can tell you with absolute certainty that effective Jan. 1 we’re going to cut and cut substantially to be below the level that we have committed to on Nov. 30," Al-Falih said Saturday in Vienna. The Saudi minister added that the country was ready to cut below 10 millions barrels a day, a level it has sustained since March 2015.Al-Falih and his Russian counterpart Alexander Novak also revealed Saturday they have been working for nearly a year on the agreement, meeting multiple times in secret. OPEC two weeks ago agreed to reduce its own production by 1.2 million barrels a day, and Saudi Arabia has long insisted that any cuts by the group be accompanied by action from other suppliers.

"The reality is both Saudi and Russia desperately need higher prices with oil their number-one export,” said Michael McCarthy, chief market strategist at CMC Markets in Sydney. “Agile U.S. shale producers will jump back into production on West Texas well before $60 a barrel.”

Data on Friday showed U.S. explorers rushed back to the shale patch with the largest weekly addition of oil rigs since July 2015. Rigs targeting crude in the U.S. rose by 21 to 498, the most since January, according to Baker Hughes Inc.